Introduction

Owning a home is one of the biggest dreams for millions of Indian families. However, increasing property prices and limited financial resources often make this dream difficult to achieve. To bridge this gap, the Government of India has introduced several housing initiatives over the years, with the Pradhan Mantri Awas Yojana (PMAY) being one of the most impactful.

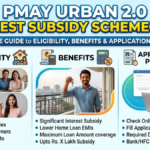

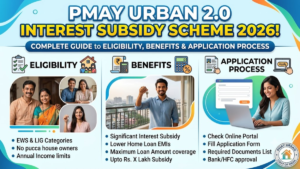

PMAY Urban 2.0 continues the government’s commitment to providing affordable housing for economically weaker and lower-income families. One of its key components is the Interest Subsidy Scheme (ISS), which helps eligible homebuyers reduce the financial burden of home loans through interest subsidies.

The scheme aims to support families from the Economically Weaker Section (EWS), Lower Income Group (LIG), and other eligible categories by making housing finance more affordable. Banks and housing finance companies, including institutions like Karnataka Bank, play an essential role in implementing the scheme by offering eligible home loans and facilitating subsidy benefits.

This article provides a comprehensive overview of PMAY Urban 2.0, its objectives, eligibility criteria, benefits, application process, and the role of financial institutions.

Understanding PMAY Urban 2.0

PMAY Urban 2.0 is a government housing initiative designed to improve access to affordable housing in urban India. The scheme focuses on helping eligible families either purchase, construct, or improve their homes through financial assistance and interest subsidies.

The Interest Subsidy Scheme is one of the most attractive features because it directly reduces the interest payable on home loans. Instead of providing cash directly, the government offers an interest subsidy that lowers the overall loan burden.

The scheme contributes to the government’s long-term vision of ensuring that every eligible urban family has access to a safe, secure, and permanent home.

Objectives of PMAY Urban 2.0

The scheme has several important goals:

- Promote affordable housing across urban India.

- Encourage home ownership among economically weaker families.

- Reduce financial pressure on first-time homebuyers.

- Support planned urban development.

- Improve living standards through better housing infrastructure.

- Increase financial inclusion by encouraging formal housing finance.

- Empower women by promoting property ownership.

- Improve access to quality housing for vulnerable communities.

What is the Interest Subsidy Scheme (ISS)?

The Interest Subsidy Scheme is a financial benefit available to eligible homebuyers who obtain housing loans through approved lenders.

Instead of paying the full interest amount throughout the loan tenure, eligible borrowers receive an interest subsidy from the government. This subsidy is credited to the loan account, reducing the principal outstanding and ultimately lowering monthly loan repayments.

Depending on eligibility and applicable guidelines, beneficiaries may receive financial assistance of up to ₹1.8 lakh under the scheme.

Key Features of PMAY Urban 2.0

Some major features include:

1. Affordable Housing Support

The scheme encourages affordable housing development in urban areas.

2. Interest Subsidy

Eligible borrowers receive financial assistance through subsidized home loan interest.

3. Financial Inclusion

The scheme promotes access to organized banking and housing finance institutions.

4. Women Empowerment

Preference is often given to families where women are property owners or co-owners.

5. Urban Development

The initiative supports planned urban growth through improved housing infrastructure.

6. Better Living Standards

The scheme promotes healthier and safer living conditions.

Who Can Benefit?

PMAY Urban 2.0 primarily targets:

Economically Weaker Section (EWS)

Families with relatively lower annual income seeking affordable housing assistance.

Lower Income Group (LIG)

Families with modest income requiring financial support for home ownership.

Other Eligible Urban Families

Subject to government guidelines and eligibility requirements.

Eligibility Criteria

Applicants generally need to satisfy several conditions.

Indian Citizenship

The applicant should be an Indian citizen.

Urban Residence

The scheme is intended for eligible urban households.

Home Ownership

Applicants should generally not own a permanent house in India, subject to scheme guidelines.

Eligible Income Category

Applicants should fall under eligible income limits prescribed by the government.

Approved Home Loan

The loan should be obtained from an approved lending institution.

Types of Housing Activities Covered

PMAY Urban 2.0 supports various housing needs.

Construction of a New House

Eligible beneficiaries may build a new house.

Purchase of a Home

The scheme supports the purchase of eligible residential properties.

Home Extension

Existing homes may be expanded to accommodate growing families.

Home Improvement

Certain improvements or upgrades may also qualify under applicable guidelines.

Financial Benefits

The scheme offers several financial advantages.

Lower Interest Burden

Government subsidies reduce overall loan costs.

Reduced EMI

Lower loan principal means smaller monthly installments.

Long-Term Savings

Borrowers save substantial amounts throughout the loan tenure.

Easier Home Ownership

Reduced financing costs make homes more affordable.

Role of Banks

Banks serve as the primary channel through which eligible borrowers access PMAY benefits.

Their responsibilities include:

- Accepting home loan applications.

- Assessing borrower eligibility.

- Processing housing finance.

- Submitting subsidy claims.

- Crediting approved subsidies to borrower accounts.

- Providing customer assistance.

Karnataka Bank’s Role

Karnataka Bank is among the financial institutions offering eligible housing loan products that may facilitate PMAY Urban 2.0 benefits for qualifying borrowers.

The bank provides:

- Home loan financing.

- Customer guidance.

- Loan processing.

- Documentation support.

- Eligibility verification.

- Assistance throughout the application journey.

Borrowers should verify the latest scheme availability and eligibility with the bank before applying.

Documents Required

Applicants generally require:

- Identity proof

- Address proof

- PAN Card

- Aadhaar Card

- Income proof

- Salary slips (if applicable)

- Bank statements

- Property documents

- Passport-size photographs

- Loan application form

Additional documents may be requested depending on individual circumstances.

Application Process

The application process generally involves the following steps.

Step 1

Choose an approved lending institution.

Step 2

Complete the home loan application.

Step 3

Submit all required documents.

Step 4

The lender evaluates eligibility.

Step 5

Loan approval is processed.

Step 6

The subsidy claim is forwarded to the appropriate authorities.

Step 7

Once approved, the subsidy amount is credited to the loan account.

Advantages for First-Time Homebuyers

PMAY Urban 2.0 offers significant benefits to first-time buyers.

These include:

- Reduced financial burden

- Affordable loan repayments

- Government-backed assistance

- Improved access to formal finance

- Greater housing security

Social Impact

The scheme contributes to broader social development by:

- Reducing housing shortages.

- Improving sanitation.

- Supporting planned urbanization.

- Creating employment in construction.

- Boosting related industries.

- Enhancing quality of life.

Economic Benefits

Affordable housing stimulates economic growth by increasing demand across multiple sectors, including:

- Cement

- Steel

- Construction

- Banking

- Housing finance

- Interior furnishing

- Home appliances

This creates employment opportunities and strengthens the economy.

Tips Before Applying

Applicants should:

- Check eligibility carefully.

- Compare loan options.

- Maintain a good credit profile.

- Keep documentation ready.

- Verify property legality.

- Understand loan repayment obligations.

- Consult the lending institution regarding current PMAY guidelines.

Common Mistakes to Avoid

Avoid:

- Submitting incomplete documents.

- Providing incorrect information.

- Ignoring eligibility requirements.

- Applying through unauthorized lenders.

- Failing to understand loan terms.

- Delaying document submission.

Why PMAY Urban 2.0 Matters

Affordable housing is more than owning property. It provides families with:

- Financial stability

- Social security

- Better education opportunities

- Improved health outcomes

- Greater community participation

- Long-term wealth creation

PMAY Urban 2.0 supports these goals by making housing more accessible to eligible urban households.

Future of Affordable Housing in India

India’s urban population continues to grow rapidly, increasing the demand for affordable homes.

Government initiatives like PMAY Urban 2.0 are expected to play a vital role in addressing this demand through financial support, improved housing infrastructure, and partnerships with banks and housing finance companies.

Continued adoption of digital processes, faster loan approvals, and enhanced financial inclusion may further improve access to affordable housing in the coming years.

Conclusion

PMAY Urban 2.0 represents a significant step toward achieving affordable housing for eligible urban families across India. Through the Interest Subsidy Scheme, the government reduces the financial burden associated with home loans, making home ownership more attainable for economically weaker and lower-income households.

By working closely with banks and housing finance institutions, the scheme ensures that eligible beneficiaries can access housing finance through an organized and transparent process. Whether constructing a new home, purchasing a house, or improving an existing property, PMAY Urban 2.0 provides meaningful financial support that can help families build a more secure future.

For prospective homebuyers, understanding the eligibility requirements, maintaining proper documentation, and approaching an approved lender are important first steps toward benefiting from the scheme. As India continues its journey toward inclusive urban development, PMAY Urban 2.0 remains an important initiative in helping millions of families realize the dream of owning a safe, permanent, and affordable home.

Note: The exact eligibility criteria, subsidy amount, income limits, and operational guidelines under PMAY Urban 2.0 may change over time. Applicants should always verify the latest information with the Government of India or their chosen lending institution before applying.